How Does NFP Affect Gold Spreads and FX Liquidity?

On the first Friday of most months, your gold and FX books get stress-tested whether you planned for it or not. In the minute before a scheduled US macro release such as Non-Farm Payrolls, high-frequency liquidity providers widen their quoted spreads by over 30% and cut top-of-book depth by a similar share, according to FCA research on GBP/USD.

For a brokerage operator, that means slippage complaints and margin events hitting several asset classes at once. The question of how NFP affects trading is usually answered for traders; this article answers it for the people running the infrastructure underneath them.

Key Takeaways

- The market reaction to the non-farm payrolls report scales with the deviation from consensus, because expectations are already priced in before 8:30 a.m. ET.

- The risk window opens on Wednesday with the ADP report, which shifts positioning and LP quoting behavior ahead of the official NFP release.

- During the release, top-of-book depth contracts first, so market orders face worse fills even when the headline spread looks survivable.

- XAU/USD degrades harder than major FX pairs, and a single-LP gold feed is the configuration most likely to fail in the first seconds.

- Aggregation architecture, quote filtering, and failover logic decide NFP-day execution quality more than any forecast does.

What NFP Measures and Why Markets React

NFP moves markets because it updates the Fed rate path in one data point. The U.S. Bureau of Labor Statistics publishes the Employment Situation report at 8:30 a.m. ET, typically on the first Friday of every month. Three numbers give desks a monthly read on the US labor market:

- the headline non-farm payrolls figure, which counts private and government employees,

- the unemployment rate,

- average hourly earnings.

The combination matters more than any single number of jobs. A payrolls beat with soft wage growth reads as economic growth without inflation pressure, so desks barely shift their monetary policy expectations. The same beat with hot wages revives the persistent-inflation scenario, and front-end yields reprice within seconds.

How Deviation From Consensus Drives Volatility

Volatility scales with the gap between the print and consensus. A 250K print against a 180K consensus is a shock; the same 250K against a 240K consensus is a rounding error. By 8:29 a.m. the consensus is already in the price, so the release only trades on what differs from it.

Big misses do outsized damage to the order book. Federal Reserve research on the interdealer FX market found that in the minute after a payrolls release, EUR/USD trading volume runs at roughly 20 times its per-minute average, a larger spike than the quarterly GDP release produces. Quoting into that surge is expensive, so market makers pull size before it arrives, and the book your clients trade into is thinnest exactly when their order flow spikes.

The Fed Policy Transmission Chain From NFP Print to USD Repricing

The chain runs in one direction. The surprise pushes rate expectations toward higher interest rates or faster cuts, those expectations move front-end Treasury yields, yields move the US dollar, and the dollar drags currency pairs and gold with it. Every link completes faster than a human can intervene, which is why the release rewards pre-configured routing logic and punishes manual reaction.

Wages complicate the picture. When payrolls and wages beat together, markets can price sticky inflation, and gold sometimes rises alongside the dollar instead of against it. An operator whose risk alerts assume a clean USD-gold inverse gets misleading signals about the central bank's next move, at the worst possible time.

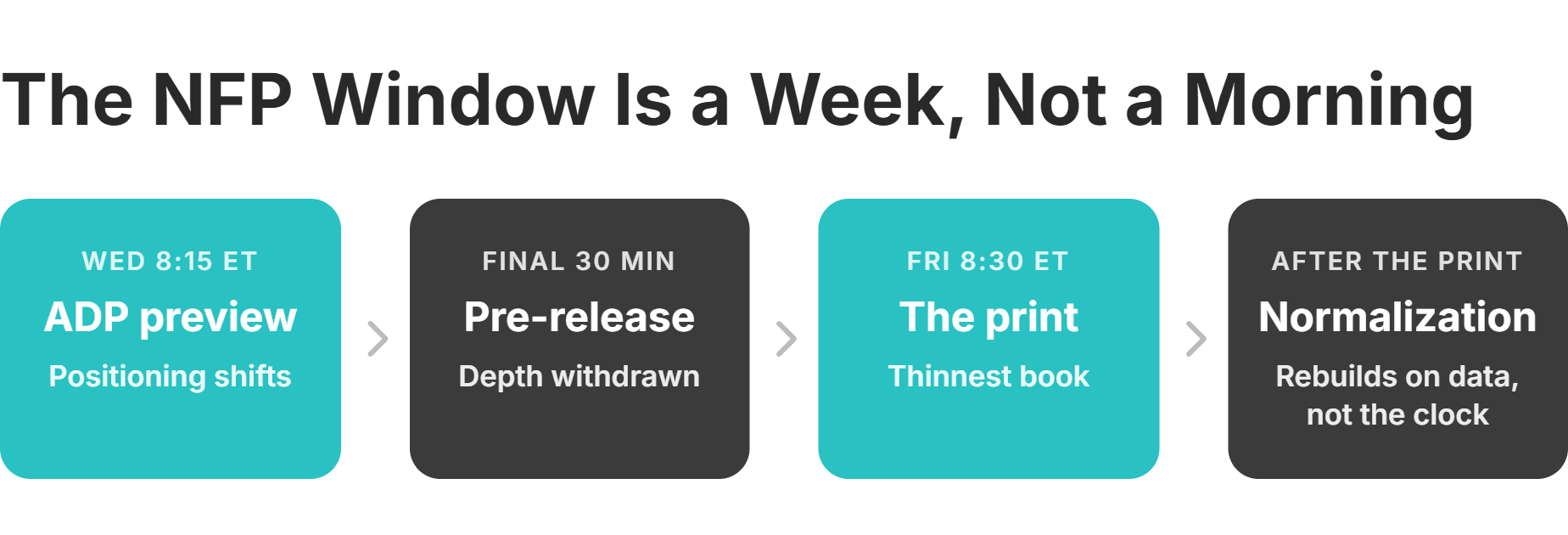

The Full NFP Event Window Brokers Must Manage

NFP week starts on Wednesday, and treating it as a Friday-morning event leaves two days of risk unmanaged. The window has three distinct phases, each with its own liquidity signature.

ADP Release as the First Volatility Trigger

The ADP National Employment Report typically lands at 8:15 a.m. ET on the Wednesday before the official print, and it is an early indicator that can shift the week's positioning. Its correlation with the BLS figure is loose, but a big ADP surprise in private-sector job growth still revises market expectations and moves the dollar and gold preemptively, giving clients a direction to trade for two extra days.

Liquidity providers watch the same early NFP data. After a strong ADP print, some begin adjusting quote parameters ahead of Friday, so spreads on Thursday can already sit wider than the weekly norm.

Pre-Release Positioning and LP Quote Behavior

The last half hour before the release is a quote-protection phase. Providers widen spreads and pull size from the top of the book to avoid being run over by the high volatility about to arrive. The FCA data cited above shows the sharpest withdrawal in the final minute, and instruments with lower baseline liquidity can thin out early.

So when the number hits, client orders route into a book that emptied itself in advance, and the first fills after the print meet very thin liquidity.

Post-NFP Normalization and Spread Recovery Timelines

Recovery times vary too much to script in advance. Research on gold futures shows the volatility impulse itself fading within a few minutes, but quoted spreads stay elevated while providers watch how price behaves at the new level, and full depth can take considerably longer to rebuild.

An outsized surprise, conflicting signals among the report's three components, and other macroeconomic releases in the same session can all stretch the timeline. A desk should re-enable normal margin and pricing parameters only after observing depth; otherwise it can do so straight into the second leg of the move.

Hold Spreads Through the Print

Keep XAU/USD and FX fills stable when individual LP feeds widen or pull quotes during the print.

How NFP Moves FX Liquidity Across Major Pairs

The release hits every USD pair, but it does not hit them equally. Reaction size and execution risk depend on each pair's baseline depth and its sensitivity to the US rate path.

How EUR/USD, GBP/USD, and USD/JPY React to a Surprise

EUR/USD is the deepest market in forex trading and still widens on the print; the depth limits slippage for forex traders on small and mid-size orders. A payrolls beat typically presses the pair lower as the dollar strengthens, and a miss lifts it.

GBP/USD runs on a thinner book, so the same surprise travels further. The first move overshoots more often than in EUR/USD, and market orders placed into the release carry visibly higher slippage.

USD/JPY refuses to follow a simple rule. A strong print usually lifts it as yields rise, but when the market reads the same print as a recession signal, safe-haven flow into the yen can offset or reverse the move. The pair's NFP reaction depends on the macro regime in force that month, so a fixed directional assumption can fail.

Liquidity Depth Deterioration and Slippage Risk During the Release Window

Depth dies from the top down. Top-of-book size contracts first, then resting orders cancel across deeper levels, and a market order that would normally fill at the touch starts walking the book. The mechanics of slippage turn nonlinear at this point. Doubling the order size can much more than double the price impact because each level consumed is thinner than the last.

For the broker, degraded fills convert directly into cost. A-book flow gets hedged at worse prices, B-book flow generates complaint tickets, and best-execution rules still demand evidence exactly when the forex market is hardest to document.

NFP Impact on Gold Spreads and XAU/USD Execution Quality

Gold is where NFP exposes weak liquidity architecture first. XAU/USD generally has less available depth than EUR/USD in normal conditions, so when providers pull the same share of quotes, gold loses more of its tradeable depth.

The USD Strength Cascade Into Gold Pricing

A strong NFP print hits gold through two channels at once, and a bigger beat in the NFP numbers deepens the move. Rising yields raise the opportunity cost of holding a non-yielding asset, and the stronger dollar can raise gold's local-currency price for many non-USD buyers, cutting demand from both directions. A weak print runs the same cascade in reverse, often amplified by a risk-off shift in market sentiment toward the metal.

The wage component can override the whole cascade. A payrolls-plus-wages beat can lift gold and the dollar together, and any alert logic built on a simple inverse will fire in the wrong direction.

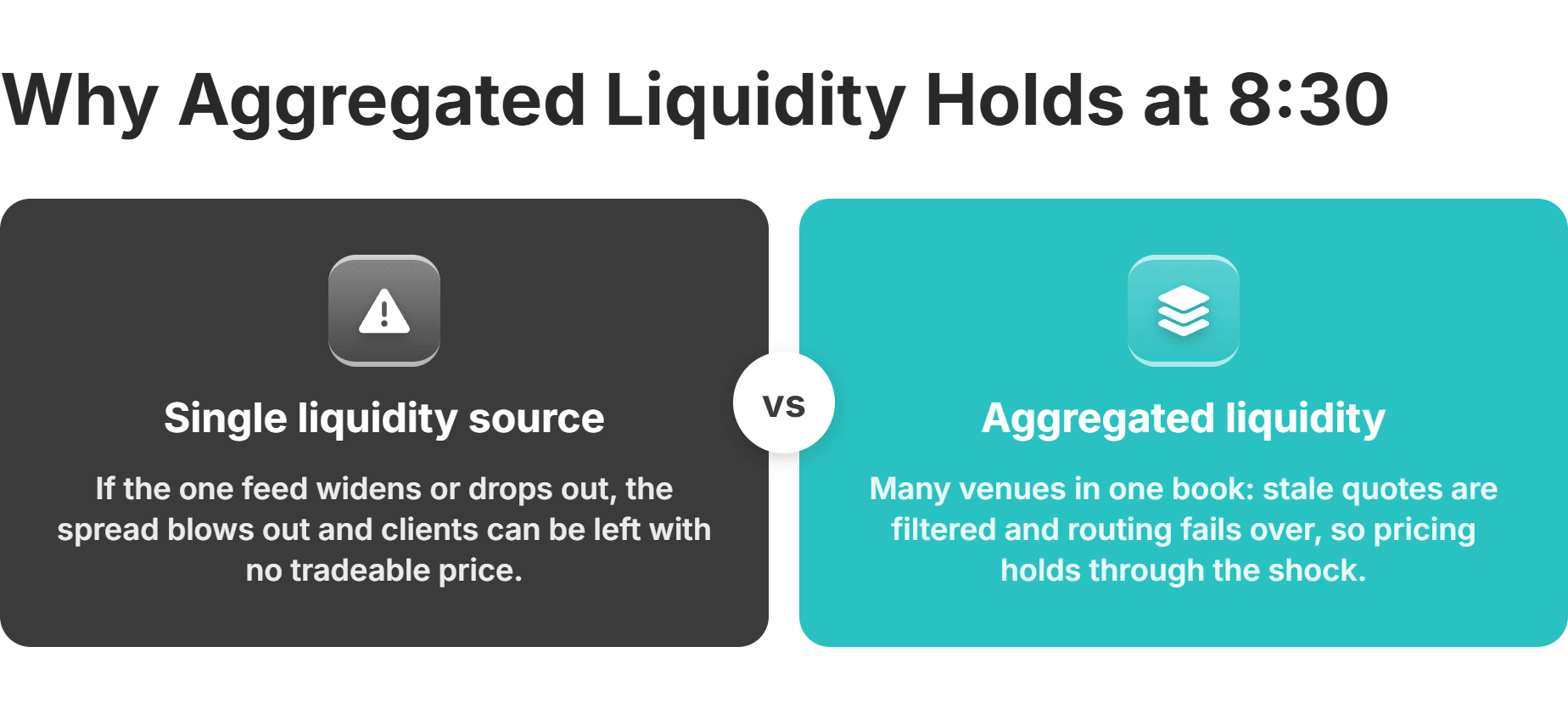

How Single-LP Configurations Amplify XAU/USD Spread Instability

A single-LP gold feed concentrates the entire event risk into one counterparty's behavior. When that provider widens sharply, every client sees the blowout at full size; if the provider pauses quoting for the first seconds of an extreme print, which does happen, the broker has no gold price at all. There is no second feed to dampen the spike and nothing to route around.

Aggregated setups degrade more gracefully. With several providers in the pool, the composite spread widens according to the best available quotes, and routing simply skips a paused feed. The same aggregation and market-depth logic applies across asset classes, but XAU/USD on NFP Friday is where its absence costs the most.

Deep, Reliable Liquidity Across 10 Major Asset Classes

FX, Crypto, Commodities, Indices & More from One Single Margin Account

Tight Spreads and Ultra-Low Latency Execution

Seamless API Integration with Your Trading Platform

NFP as a Cross-Asset Infrastructure Stress Event

NFP stresses the whole brokerage at once, because a single rate-path revision reprices every asset class simultaneously. At 8:30 a.m., FX majors, XAU/USD, equity index futures, and Treasury futures all move on the same surprise.

Correlated Volatility Spikes Across FX, Gold, Equities, and Bonds

The correlation comes from portfolio structure. Institutional portfolios span asset classes, so one revision to the Fed rate path re-marks all of them across financial markets within seconds, and a multi-asset broker absorbs those flows through the same liquidity layer, margin engine, and support queue.

That concentration is the real operational risk. Volatility in EUR/USD triggers margin events in accounts denominated in other currencies, and cross-border liquidity management across time zones determines whether those parallel events resolve cleanly or pile up. Treating NFP as just an FX pricing issue understates how much load this read on the U.S. economy puts on everything downstream.

Operations teams need one release playbook across pricing, margin, and support. It should cover depth monitoring across the affected books, pre-event capacity tests, and the routing of client inquiries before they become an incident queue.

Keep Margin Controls Synchronized

See every account currency in one back office when FX, gold, and indices reprice together on release day.

How Liquidity Aggregation Architecture Determines NFP-Day Execution Quality

By Friday morning, your execution quality is already decided for every client who will trade NFP that day. How NFP affects trading on your platform is a property of the aggregation setup, configured earlier and under calm market conditions.

The evaluation questions are concrete. How many independent price sources feed each instrument, gold included? What happens to the composite when one source widens tenfold? How quickly does the system exclude a stale feed, and does that happen automatically or only when a human notices?

Routing Around Degraded LP Feeds to Maintain Pricing Continuity

An aggregation layer with smart routing compares live quotes across providers and fills against the tightest available price, so one provider's blowout stays that provider's problem. Quote filtering adds the second layer of protection by dropping feeds that stop updating during the fast market, which prevents a frozen price from reaching clients as a tradeable quote.

Source weighting closes the loop over time. After each release, the desk can demote the providers that widened worst before the next event window.

Build Your NFP-Ready Infrastructure Before the Next Release

NFP publishes the weaknesses already present in your setup, on a fixed monthly schedule. The pricing questions from the previous section are half of the pre-release review; the other half is whether margin capacity covers correlated multi-asset volatility and whether the back office sees every account currency in one place while it happens.

A brokerage can assemble that resilience through one integrated stack. Multi-Asset Liquidity from B2BROKER delivers aggregated pricing across ten asset classes, from the gold and FX books NFP hits hardest to index CFDs, while the B2TRADER trading platform and B2CORE back office keep execution and margin controls on the same rails during the spike.

The next NFP report is already on the economic calendar, which makes this one of the few stress tests you get to prepare for in advance. B2BROKER's team can review how NFP affects trading conditions on your platform and close the gaps before the next first Friday.

Prepare Before the Next Friday

Review pricing, platform capacity, and back-office controls together before the next NFP Friday hits.

Frequently Asked Questions about NFP in Trading

- What is NFP, and why does it move markets?

NFP is the monthly US Employment Situation report, published by the Bureau of Labor Statistics at 8:30 a.m. ET, typically on the first Friday. Markets move when the print misses consensus, because that miss reprices Fed rate expectations and flows through yields into the dollar, FX pairs, and gold within seconds.

- How does NFP affect forex pairs?

A stronger-than-expected print typically lifts the USD, pressing EUR/USD and GBP/USD lower, while a weak print does the opposite. Execution conditions deteriorate across all majors during the release window as providers widen spreads and cut depth, with thinner pairs degrading more.

- How does NFP affect gold?

Gold usually trades inversely to the dollar around NFP, so a strong print pressures XAU/USD and widens its spread sharply. Setups running a single gold liquidity provider are the most exposed, while aggregated multi-source pricing keeps a usable quote alive when individual feeds widen or pause.

- Is it good to trade during NFP?

The first impulse after the print is the highest-risk moment, with spreads at their widest and false breakouts common. Traders who wait for depth to rebuild, or cut size and tighten risk management parameters, keep execution costs from consuming the trade.

- How can brokers prepare for NFP volatility?

Treat NFP as a scheduled stress event across pricing, margin, and client support. Review LP configuration, routing logic, and margin capacity before the release, and brief support teams on spread-related inquiries in advance.