AML and KYC for Brokers: How to Build Compliant Operations

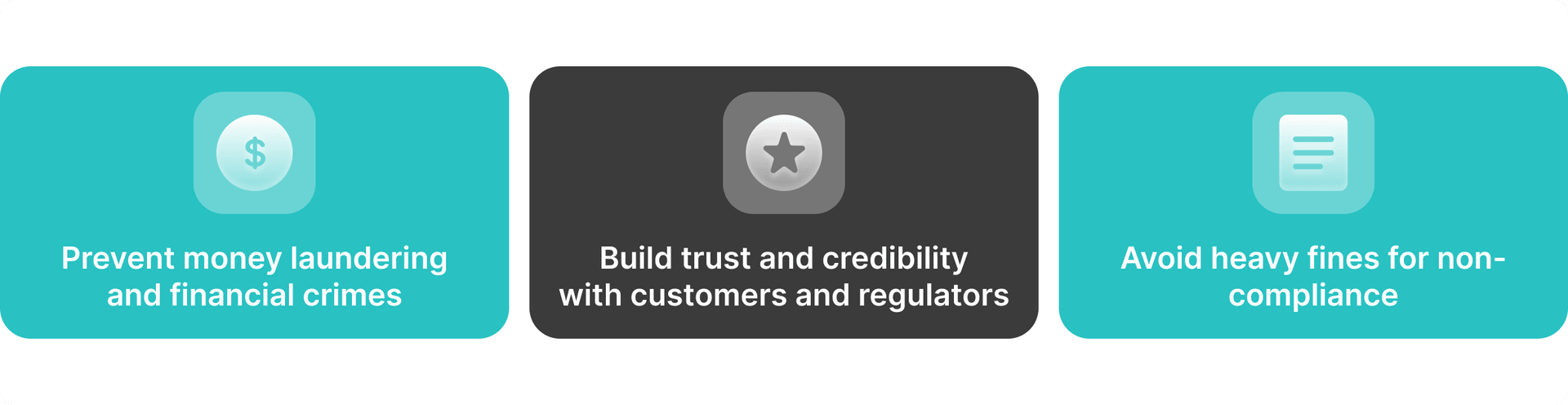

AML and KYC are unavoidable requirements for brokers seeking to attract new clients, jurisdictions, and financial partners. Every regulated trading platform must verify customer identities, monitor activity, and demonstrate effective controls to regulators and banking institutions.

Many platforms perceive KYC/AML regulations as a source of friction in the financial market, while in fact the biggest cracks come from poor implementation, operational drag, and fragmented systems. So, how can brokers meet regulatory expectations without sacrificing scale or client experience?

In this guide, we will focus on Know-Your-Customer and Anti-Money Laundering programs, their challenges, and the building blocks of a robust compliance infrastructure.

Key Takeaways

- AML and KYC are compliance systems that scale with trading activity, not static onboarding checks.

- Poorly integrated compliance tools increase friction, false positives, and operational risk.

- Modern AML/KYC programs balance automation with human oversight.

- Modern brokerage solutions embed compliance directly into the technology stack.

Discover the Tools That Power 500+ Brokerages

Explore our complete ecosystem — from liquidity to CRM to trading infrastructure.

Why AML and KYC Are Harder for Brokers Than Other Financial Firms

AML (Anti-Money Laundering) and KYC (Know Your Customer) are challenging concepts for trading platforms because they operate in a highly vibrant environment, dealing with retail traders, institutional investors, liquidity partners, payment processors, and other financial service providers.

Unlike traditional banks or hedge funds, brokers manage real-time market exposure, leverage, trading strategies, and margin trading that generate complex risk signals. Moreover, client behavior, trading frequency, deposits and withdrawals, position sizing, and margin usage make KYC and AML compliance programs more nuanced.

Cross-jurisdictional operations and onboarding clients from different regulatory frameworks add overlapping AML/KYC obligations, requiring a consistent compliance infrastructure that aligns with multiple regions rather than a single rulebook.

Finally, funding methods, such as credit/debit cards, bank transfers, e-wallets, and crypto storage, introduce further complexity and monitoring requirements.

The Bank Secrecy Act (BSA) is a US AML law enacted in 1970 that requires financial institutions to report cash transactions over $10,000, file Suspicious Activity Reports (SARs), and maintain records to help prevent money laundering and financial crime.

The Core Building Blocks of a Broker AML/KYC Program

Regardless of jurisdiction or size, every AML/KYC program relies on interconnected components that work together rather than in isolation.

Client Identification and Risk Profiling

The core function is client due diligence, which verifies identity, establishes baseline risk profiles during onboarding, and screens clients against sanctions lists and politically exposed persons lists.

This process is crucial for complying with FinCEN requirements to combat financial crime and avoid terrorist financing.

Enhanced due diligence determines how clients are monitored over time. It also influences alert thresholds, review frequency, transaction limits, and escalation paths. Therefore, weak classification can result in unnecessary alerts for low-risk clients, disrupting the user experience and delaying the detection of higher-risk behavior.

Ongoing Monitoring and Escalation

Continuous monitoring is the operational core of AML. For brokers, this includes observing funding activity, withdrawals, cross-account exchanges, and trading behavior against expected patterns.

Effective transaction monitoring depends on clear rules and consistent documentation. High alert volume alone does not indicate effectiveness because false positives exist. Therefore, a program’s success is only measured by explainable decisions supported by evidence and audit trails.

Get a Pre-Integrated Trading Platform

Streamline AML and KYC seamlessly with B2BROKER’s white-label infrastructure

How Global Regulations Shape Broker AML/KYC Requirements

Multi-market brokers must design KYC/AML modules that align with overlapping regulatory expectations and evolving laws. While specific requirements vary by jurisdiction, financial authorities expect the following:

- Consistent application of policies across clients and regions.

- Clear documentation of decision-making processes and reviews.

- Explainable control paths rather than obscure automation.

- Evidence of intended system design and actual outcomes.

From an operational perspective, this means brokers must prioritize the unified synchronization of the compliance infrastructure, rather than activating individual tools, especially when operating in multiple regions and jurisdictions.

What a Modern Broker Onboarding Flow Looks Like

The modern onboarding process balances compliance requirements with client experience. The goal is not to remove friction entirely, but to apply proportional scrutiny at each stage.

From Identity Verification to Trading Enablement

A well-designed customer identification program puts clear operational separations between steps without creating UI/UX gaps. As such, each stage of the following fulfills specific compliance needs.

- Data capture and customer due diligence

- Risk screening against PEP watchlists.

- Risk-based approval and profiling.

- Account activation with relevant controls and limits.

- Access to trading based on risk profile and jurisdiction requirements.

It is worth noting that automation plays a key role in speed and consistency, particularly for low- and medium-risk clients. However, this does not mean eliminating human intervention, which is still needed for deep analysis, case judgment, contextual review, and documented decisions.

Where AML and KYC Programs Commonly Break Down

As platforms scale, KYC/AML modules face systemic errors that may hinder the broker’s growth. These issues include:

Over-reliance on manual processes: poorly tuned rules generate excessive alerts, overwhelming compliance officers, and slowing down onboarding. This leads to teams spending more time clearing low-risk cases instead of focusing on meaningful decision-making.

Fragmented systems: when CRM platforms, trading systems, and AML tools are weakly integrated, data becomes inconsistent. This leads to duplicate workflow, unclear context, and incoherent audit trails.

Build a Unified Trading Infrastructure

Customize your brokerage platform with pre-built compliance systems, liquidity access, payment providers, and more, in one solution

Broker-Specific Red Flags Compliance Teams Should Watch

Trading environments come with common risk assessment practices that most brokers are aware of and prepare for. These include observing suspicious transactions, funding methods, and account activity.

Brokers must configure automated thresholds to observe these patterns and escalate them in a timely manner before they lead to serious issues. Moreover, admins must set reasonable escalation thresholds and paths and disclose them to regulatory bodies when requested.

Evaluating AML and KYC Solutions for Broker Use Cases

Choosing an AML and KYC solution is a core infrastructure decision for brokers. The right compliance setup directly affects onboarding speed, operational cost, regulatory confidence, and scalability.

At the same time, most AML/KYC platforms are built for static financial institutions, while brokerage firms operate in a dynamic environment shaped by trading behavior, leverage, news events, and multi-asset exposure.

These factors require brokers to carefully evaluate solutions based on how well they integrate into their systems and support ongoing risk management. Let’s discuss key evaluation points.

Integration With the Broker Technology Stack

Integration depth often determines whether an AML/KYC solution reduces or increases operational work—a key factor for a broker’s automation. Compliance decisions rely on timely data pulled together from CRM systems, trading platforms, financial transactions, and client screenings.

Deeply integrated solutions ensure smooth data ingestion between connected tools that work together as a single unit. In contrast, weak integrations lead to duplicated data, delayed alerts, and incompatible audit trails.

In a nutshell, it is not about having an integration; it is about how well these integrated instances work together.

Support for Trading Activity and Multi-Asset Risk

Compliance solutions designed for banks and traditional firms often struggle to cope with dynamic trading behavior. Therefore, brokers must evaluate whether platforms can contextualize their objectives and funding patterns and adapt their logic to leverage, scale, and manage risk profiles.

This capability is particularly vital for broker-dealers operating across Forex, CFD, crypto, and other financial instruments, where risk characteristics differ significantly.

Scalability Across Volume, Clients, and Jurisdictions

Scalability in AML and KYC is often misunderstood. While transaction volume matters, brokers must also consider how solutions perform as onboarding accelerates, client numbers increase, and regulatory exposure expands.

Many platforms function well at low volume but struggle as alert queues grow, review times increase, and workflows become congested, amplifying financial and reputational damage.

Therefore, brokers should assess how the solution manages activity peaks, such as during marketing campaigns or market-driven trading surges. Performance degradation during these periods can quickly translate into delayed account approvals and lost revenue.

Jurisdictional scalability is equally important. When brokers expand into new regions, they need AML/KYC systems that support additional regulatory requirements without forcing a complete redesign of workflows.

Alert Quality, Transparency, and Explainability

The effectiveness of an AML/KYC compliance solution is not measured by how many alerts it generates, but by how useful those alerts are. Excessive false positives drain resources and reduce the team’s ability to focus on genuine high risk.

Brokers should examine how alerts are generated and prioritized, and whether the reasoning behind each alert is clear.

This is why explainability is critical; compliance teams must justify decisions to regulators, auditors, and banking partners. Alerts that cannot be clearly explained increase investigation time and introduce inconsistency.

Transparent alert logic also improves internal alignment, providing clear evidence of why a case was flagged, enabling teams to apply judgment more confidently and document decisions more effectively. Over time, this leads to fewer unnecessary reviews and a stronger compliance backbone.

Workflow Support for Review, Escalation, and Reporting

Streamlining AML and KYC practices relies on internal teams and legal officers making informed decisions, supported by structured workflows. Therefore, a strong solution provides the following tools to brokers:

- Clear case management workflow: Structured processes that guide investigation, escalation, and resolution consistently.

- Audit trails showing reviewers and timestamps: Automatic recordkeeping demonstrates accountability and supports audits.

- Support for regulatory reporting and internal oversight: Built-in reporting reduces manual effort and improves visibility.

Long-Term Operational and Cost Impact

Upfront licensing fees tell only part of the story. Brokers should evaluate the long-term operational impact of an AML/KYC solution, including its effects on staffing, review time, integration, and maintenance. For example:

- False positives: Excessive alerts increase manual review time, operational workload, and onboarding delays.

- Ongoing integration maintenance: Weak integrations require constant updates as systems evolve, taking up resources and time.

- Incremental costs as volume grows: Costs rise as brokers scale with more clients, alerts, and transactions.

Therefore, brokers must evaluate the value of beneficial ownership when selecting a KYC/AML provider. Solutions that appear cheaper initially can become expensive as clients, assets, and regulatory exposure increase.

Vendor Maturity and Ongoing Support

KYC and AML requirements evolve continuously, especially for brokers expanding into new markets or offering new products. Therefore, vendor maturity plays a critical role in how well a solution adapts to these changes.

Brokers should partner with vendors that update their platforms in response to regulatory developments, and respond promptly during audits or compliance incidents. You must ensure clear communication channels for product direction and the roadmap, and define accountabilities and responsibilities.

Ultimately, AML and KYC solutions are not one-time purchases. They are long-term partnerships that shape how brokers manage risk, satisfy regulators, and support growth over time.

Enabling Growth While Staying Regulator-Ready

AML and KYC do not have to slow brokers down. When designed as part of the brokerage stack, compliance supports faster onboarding, operational resilience, and sustainable growth.

Reliable brokerage solution providers offer robust compliance systems that treat anti-money laundering and know-your-customer protocols as a unified, embedded, scalable infrastructure aligned with the broker’s objectives.

Build a compliant broker infrastructure with B2BROKER, and get pre-integrated KYC/AML modules, advanced risk management tools, and top-notch execution engines that get you competitive from day one.

Have a Question About Your Brokerage Setup?

Our team is here to guide you — whether you're starting out or expanding.

Frequently Asked Questions about AML and KYC Compliance for Brokers

- Can AML and KYC be automated without increasing regulatory risk?

Yes, when automation is implemented with clear rules, explainable alerts, and human oversight. Automation should handle data collection and screening, while compliance teams retain control over reviews, escalation, and reporting decisions.

- How do brokers evaluate whether an AML/KYC solution will scale with growth?

Scalability depends on more than transaction volume. Brokers should assess whether a solution can handle higher onboarding throughput, additional asset classes, new jurisdictions, and increased alert volumes without degrading performance or requiring manual workarounds.

- Why is integration with trading platforms and CRM systems so important?

AML and KYC decisions rely on accurate, timely data from client onboarding, funding, and trading activity. Weak or partial integrations create data gaps that lead to false positives, delayed reviews, and audit issues.

- What should brokers look for when comparing AML/KYC vendors?

Key criteria include integration depth, support for trading-specific risk, alert transparency, workflow support for investigations, and predictable long-term costs. The best solutions fit naturally into the broker’s existing technology stack.

- How can brokers measure whether their AML/KYC program is working?

Beyond passing audits, brokers should track onboarding speed, compliance cost per client, alert quality, and confidence from regulators and banking partners. These metrics indicate whether compliance supports growth or creates friction.

- Do AML and KYC tools replace in-house compliance teams?

No. AML/KYC tools support compliance teams by automating repetitive tasks and improving consistency. Human judgment remains essential for interpreting alerts, making escalation decisions, and maintaining regulatory relationships.