Latency Arbitrage Explained for Institutional Brokers

At its core, latency arbitrage exploits microsecond delays in how price quotes spread across fragmented markets. For brokers and dealing desk teams, it directly impacts execution quality, creates toxic order flow, and increases risk.

Rather than being just another trading tactic, latency arbitrage poses a serious competitive challenge that requires substantial infrastructure upgrades and careful planning for brokerage integrations.

In this article, we dig into how arbitrageurs profit from stale quotes and what that does to your spreads and slippage. We then trace the slowdowns in your trading systems and lay out the technology defenses that actually work.

Key Takeaways

- The latency arbitrage strategy exploits microsecond gaps between different exchange feeds and price data, enabling fast traders to profit from old quotes while slower users can’t keep up.

- Physical distance, network routing, and matching-engine queue times are the primary sources of latency that create exploitable price discrepancies in multi-asset trading infrastructure.

- Technology controls such as quote throttling, last-look filters, and real-time toxic flow analytics help brokers detect and block latency arbitrage before it erodes execution quality.

- Selecting liquidity providers with transparent toxic flow reporting, co-location options, and anti-latency-arbitrage mechanisms is critical for maintaining fair execution and competitive spreads.

What Is Latency Arbitrage, and Why Should Brokers Care?

Latency arbitrage is a high-speed trading strategy that exploits microsecond delays in price quote dissemination across fragmented financial markets.

When one exchange updates its price before another, a fast trader can buy at the stale (lower) price and sell at the updated (higher) price, locking in a near-riskless profit. The entire transaction often completes in less time than it takes a human eye to blink.

For institutional brokers, dealing desk heads, and risk managers, this is not just a curiosity from the world of algorithmic trading. It is a predictable execution-quality problem that quietly makes your client flow toxic and inflates dealing risk.

Every time a latency arbitrageur picks off one of your stale quotes, your firm absorbs a loss that compounds across thousands of daily executions.

This practice is especially common in Forex, equities, and cryptocurrency markets, where liquidity is fragmented across many venues and speed asymmetries create persistent opportunities.

Understanding the mechanics, knowing where the vulnerabilities sit in your own infrastructure, and building the right defenses around them is what separates a brokerage that controls its execution quality from one that bleeds margin to faster participants.

Why Direct Feeds Beat Aggregated Feeds Every Time

The core vulnerability behind latency arbitrage comes down to how price data reaches different market participants. Direct exchange feeds deliver raw market data with minimal latency, often in single-digit microseconds.

On the other hand, aggregated feeds collect prices from multiple sources, normalize them, and redistribute them with processing delays that can range from 1 to 10 milliseconds. That gap might sound trivial, but it is where the money lives.

High-frequency trading firms subscribe to direct feeds from individual venues, enabling them to see price changes before the consolidated National Best Bid and Offer reflects the update. A broker relying on an aggregated feed is, by definition, looking at yesterday’s newspaper while the arbitrageur reads tomorrow’s headline.

For brokers who aggregate liquidity from multiple sources, this creates a structural disadvantage. Your quoted prices inevitably lag the true market, and anyone with a faster feed can see the discrepancy and trade against it before your system catches up.

The result is a steady drip of adverse fills that may not look alarming on any single trade but compound into significant P&L drag over time.

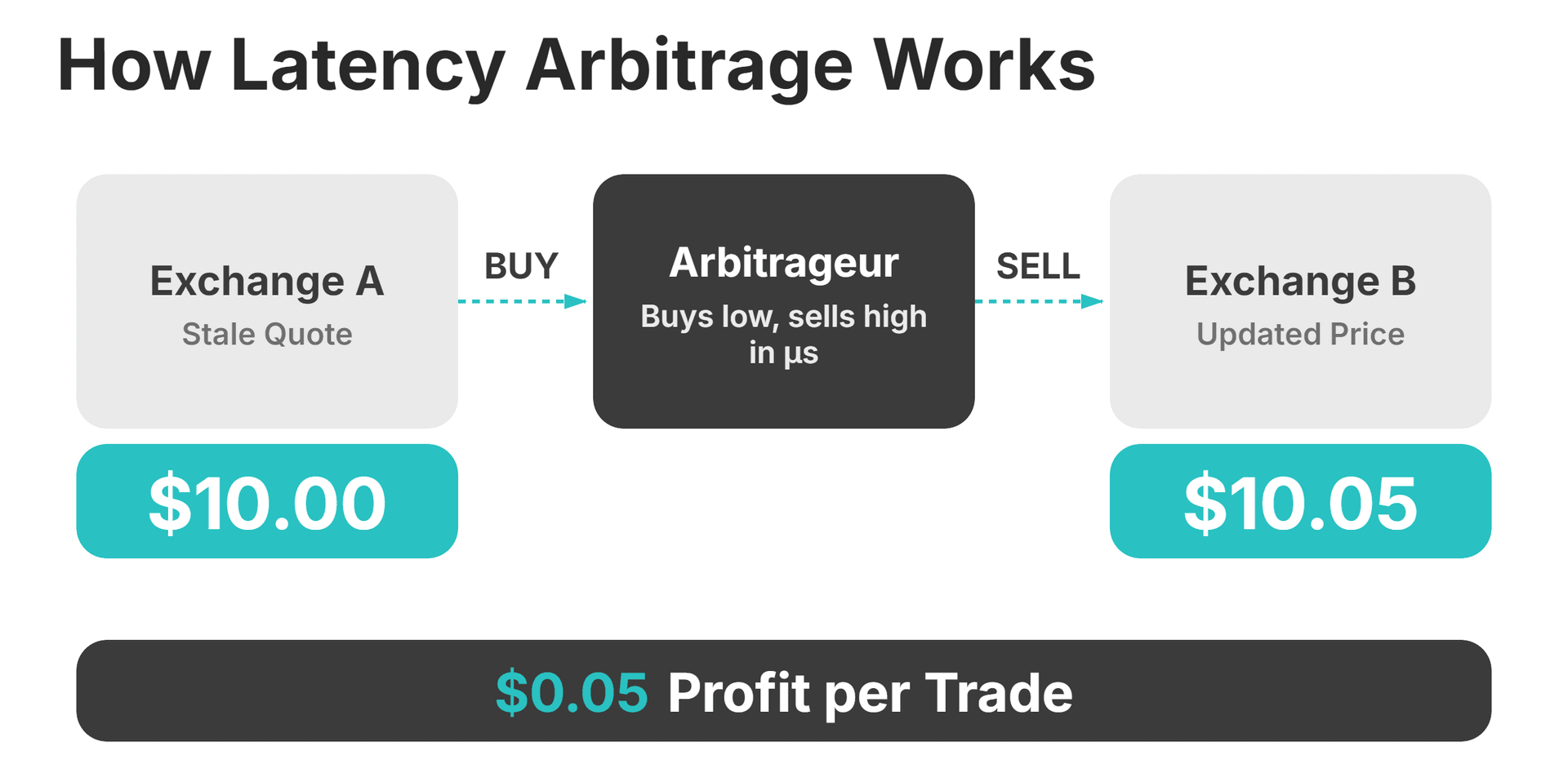

How a Latency Arbitrage Trade Unfolds in Microseconds

A typical latency arbitrage trade follows a four-step workflow that plays out in microseconds.

- First, the arbitrageur detects a price movement on Exchange A via a direct feed.

- Second, their algorithm calculates that Exchange B’s quote has not yet been updated and is still showing a stale price.

- Third, the algorithm submits an executable order to Exchange B at that stale price.

- Fourth, the trade executes before Exchange B’s quote refreshes, capturing the price difference as profit.

Because the arbitrageur exploits a known price discrepancy rather than speculating on future movements, the market risk is minimal. This is not a bet on direction; it is a systematic extraction of value from slower participants.

The entire sequence occurs faster than traditional monitoring systems can register it, which is exactly why so many brokers only realize they have a problem when their spread performance deteriorates, or their risk book starts behaving unpredictably.

This workflow connects directly to the concept of picking off liquidity. Passive orders from brokers and market makers become targets for systematic exploitation, turning what should be healthy client flow into a one-sided drain on your bottom line.

How Latency Arbitrage Turns Your Client Flow Toxic

Toxic flow is order flow that consistently results in adverse selection, meaning the trades move against the broker immediately after execution.

Latency arbitrageurs generate toxic flow by systematically targeting brokers’ stale quotes, forcing firms to fill orders at prices that are already outdated by the time the trade settles.

The pattern is unmistakable once you know what to look for. Toxic flow clusters around price update events, shows a consistently adverse trade direction, and comes from counterparties with an HFT or algorithmic profile.

You will also see systematic losses, wider spread requirements, and short time-to-adverse-movement after fills. Compare that to natural flow, which is randomly distributed throughout the trading session, comes from retail traders and institutional clients, and shows balanced wins and losses with standard competitive spreads.

This is a structural problem that demands infrastructure-level solutions. No amount of manual dealing desk intervention can outpace algorithms operating in microseconds.

Brokers who fail to address latency arbitrage face a compounding disadvantage: wider spreads to compensate for losses, which drive away legitimate client flow, further concentrating the toxic share of remaining volume.

Power your Brokerage with Next-Gen Multi-Asset & Multi-Market Trading

Advanced Engine Processing 3,000 Requests Per Second

Supports FX, Crypto Spot, CFDs, Perpetual Futures, and More in One Platform

Scalable Architecture Built for High-Volume Trading

Where Latency Actually Comes From (And Where You’re Most Exposed)

Understanding the source of latency helps brokers identify vulnerabilities and prioritize infrastructure investments. Latency accumulates across multiple points in the trading chain, from market data transmission to order execution confirmation, and every added millisecond creates a wider window for exploitation.

Physical Distance and Network Routes

The speed of light imposes hard limits on data transmission. A signal traveling from Chicago to New York takes approximately 7 milliseconds via standard fiber optic routes, which is an eternity in high-frequency trading.

Co-located HFT firms position their servers within the same data center as exchange matching engines, reducing round-trip latency to microseconds.

Geographic dispersion across multiple liquidity venues compounds the challenge for brokers aggregating prices from global sources. Network routing decisions, whether you use fiber, microwave, or multi-hop connections, create measurable latency differences that arbitrageurs exploit.

Co-location and optimized network routing are baseline requirements for any broker seeking to reduce their latency exposure.

Feed Processing and Aggregation Delays

Even after data arrives, processing it takes time. Legacy systems with inefficient architectures introduce unnecessary overhead compared to modern, purpose-built trading infrastructure.

Liquidity aggregation itself introduces latency because consolidating prices from multiple sources requires computation time before the best bid and offer are available to quote.

B2BROKER’s institutional-grade infrastructure minimizes processing delays through optimized feed handling and low-latency aggregation, naturally reducing the window that arbitrageurs need to exploit stale prices.

Outpace Arbitrageurs With Ultra-Fast Aggregation

Upgrade to our low-latency matching engine and aggregation technology to execute trades before prices go stale.

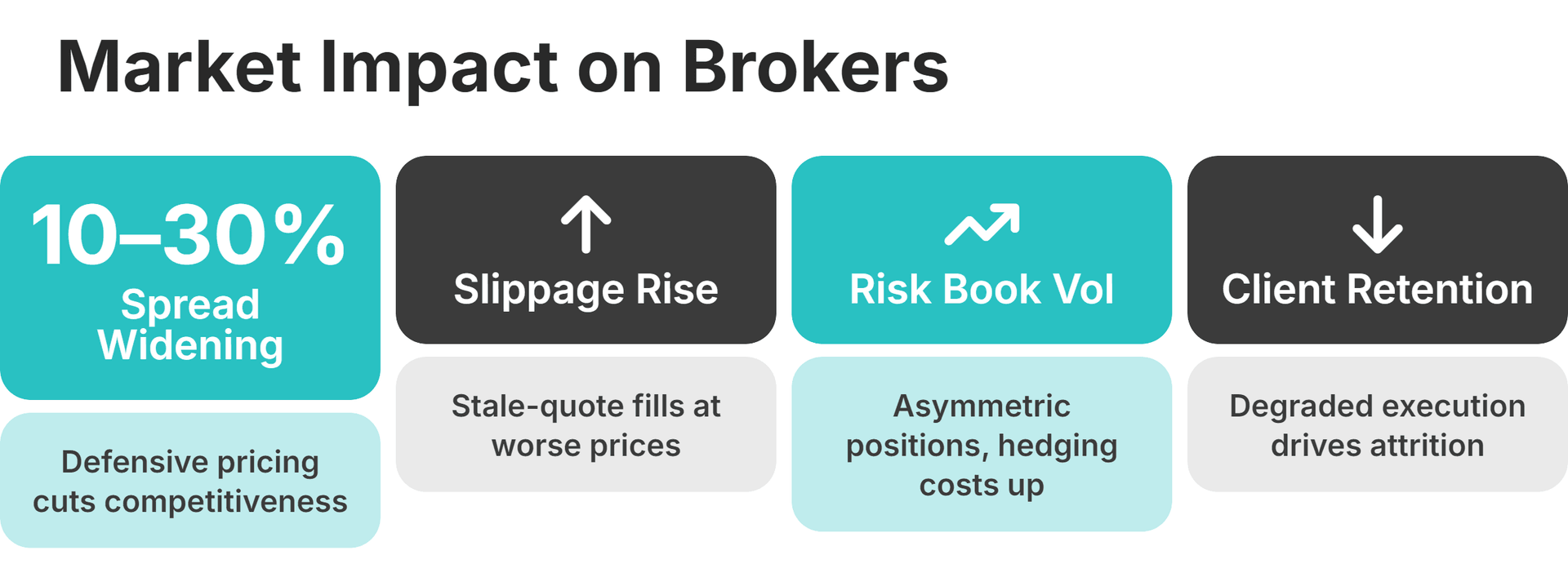

Market Impact on Spreads, Slippage, and Risk Books

Latency arbitrage has measurable effects on three key broker metrics: bid-ask spreads, execution slippage, and risk book volatility.

Spread widening occurs when market makers and brokers defensively widen their quotes to offset losses from toxic flow. If a significant portion of your incoming orders are adverse, you have to build a cushion into your pricing.

Slippage increases because latency arbitrageurs specifically target moments of price transition. When your quotes are stale by even a few milliseconds during a fast-moving market, the fills you provide are consistently on the wrong side of the new price.

Risk book volatility grows as the directional concentration of toxic flow builds asymmetric positions in your risk book faster than your hedging algorithms can offset them.

These impacts compound over time, and failing to address latency arbitrage creates structural disadvantages against competitors with superior infrastructure, widening the execution quality and client retention gaps.

How to Detect and Block Latency Arbitrage Before It Costs You

Technology-based countermeasures are the primary defense against latency arbitrage. Effective controls operate at multiple levels, from exchange-level mechanisms to liquidity provider filters and broker-side analytics.

No single control eliminates latency arbitrage entirely, but layered defenses provide the most robust protection.

Quote Throttling and Exchange Speed Bumps

Quote throttling limits how frequently a market maker can update their quotes, reducing the speed advantage of direct-feed arbitrageurs. Exchange speed bumps are intentional delays, typically 350 microseconds, applied to incoming orders, giving liquidity providers a brief window to update quotes before arbitrage orders execute.

Not all exchanges implement speed bumps, so brokers should prioritize venues with anti-latency-arbitrage mechanisms when routing orders.

Last-Look Filters and Reject Logic

Last-look is a liquidity provider’s ability to review and potentially reject orders during a brief window, typically 10 to 200 milliseconds, before execution.

It is one of the most effective protections against latency arbitrage in the Forex market, giving LPs time to check whether the requested price still reflects current conditions.

Applied too aggressively, last-look can disadvantage legitimate traders and reduce fill rates. For this reason, liquidity providers with transparent last-look policies help brokers understand execution terms and set appropriate client expectations.

Last look shapes forex execution more than most traders realize. Learn how it works, why it exists, and when it impacts pricing and fills.

Real-Time Toxic Flow Analytics

Real-time analytics platforms monitor order flow patterns to identify toxic flow signatures, including clustering around price updates, consistent adverse selection, and algorithmic timing patterns.

Brokers can tag and track counterparties exhibiting toxic flow characteristics, enabling targeted risk-management responses beyond blanket spread widening.

Key metrics to watch include fill-to-mid ratios, time-to-adverse-movement, and counterparty profitability distributions. When these metrics skew consistently against your book, it is a clear signal that latency arbitrage may be present. Dealing desks can automate alerts to respond quickly, adjusting exposure limits or routing rules before losses accumulate.

Stop Bleeding Margin to Toxic Flow

Connect to our institutional Prime of Prime liquidity pools equipped with advanced toxic flow filtering and transparent reporting.

What to Ask Your Liquidity Provider

Your liquidity provider’s infrastructure and transparency practices are as important as their protective mechanisms when onboarding or reviewing LP relationships. Here is a practical checklist of questions that matter.

Co-Location and Connectivity

Ask whether your LP offers co-location options that enable your trading infrastructure to sit close to matching engines. Cross-connect availability within data centers, where direct fiber connections eliminate network hops and reduce round-trip latency, is a meaningful differentiator.

Geographic diversity matters too. Providers with presence in major financial centers like London, New York, Tokyo, and Singapore reduce latency to regional liquidity pools.

FIX protocol support with optimized messaging reduces processing overhead compared to proprietary APIs.

Reporting Transparency

Reputable liquidity providers offer detailed real-time toxic flow metrics, enabling brokers to quantify exposure and identify trends. Request access to reject rates, fill-to-mid ratios, time-to-adverse-movement distributions, and counterparty-level profitability analysis.

Providers should also offer real-time dashboards and historical reporting for compliance and risk management purposes. Transparency indicates a provider’s confidence in their execution quality, and any reluctance to share metrics is a red flag that deserves scrutiny.

Is Latency Arbitrage Legal? The Regulatory Picture

Latency arbitrage occupies a legal gray area. It is not explicitly illegal in most jurisdictions, but regulators increasingly scrutinize its market impact. The core concern is that latency arbitrage may undermine market fairness, disadvantage institutional and retail investors, and reduce overall market integrity.

Some jurisdictions have implemented or proposed rules targeting HFT practices, including transaction taxes, minimum resting times, and speed bump requirements.

Supporters of latency arbitrage argue that it improves price discovery and liquidity by quickly correcting cross-market discrepancies. The reality, however, is more nuanced than either side suggests.

For brokers, the legal question matters less than the practical one. Regardless of legality, you have a responsibility to protect client execution quality from systematic exploitation. Brokers should ensure their practices and counterparty relationships align with evolving compliance requirements while implementing the technical defenses described above.

Your Next Steps Toward Cleaner, Fairer Execution

Latency arbitrage is not going away. As markets become faster and more fragmented, the incentives for speed-based exploitation only grow. However, brokers who invest in anti-latency-arbitrage infrastructure today position themselves for sustainable growth in increasingly competitive markets.

B2BROKER is a technology and liquidity partner that provides institutional-grade infrastructure designed to minimize latency arbitrage exposure. The comprehensive ecosystem includes multi-asset liquidity aggregation, low-latency connectivity, risk management tools, and transparent reporting, all integrated in a single layer.

Shield Your Brokerage From Predatory Algorithms

Book a demo to discover how B2BROKER’s solutions can accelerate your financial business.

Frequently Asked Questions about Latency Arbitrage

- What is latency arbitrage trading?

Latency arbitrage is a high-frequency trading strategy that exploits microsecond delays in price updates across different exchanges. Fast traders use these delays to buy or sell at stale prices before slower brokers can update their quotes.

- Is latency arbitrage illegal?

Latency arbitrage is generally not illegal, but it exists in a regulatory gray area. Many regulators heavily scrutinize the practice, and some exchanges have introduced artificial "speed bumps" to reduce its effectiveness and protect market integrity.

- What metrics signal latency arbitrage targeting my brokerage?

Key warning signs include a persistently poor fill-to-mid ratio, immediate adverse price movements right after an order fills, and unusual clusters of trades exactly when market prices update. A sudden, unexplained widening of your risk book's P&L against specific counterparties is also a massive red flag.

- Which asset classes are most vulnerable to latency arbitrage?

Forex, equities, and cryptocurrencies are highly vulnerable because their liquidity is heavily fragmented across dozens of different exchanges and venues worldwide. Any market that lacks a single, centralized pricing feed is a prime target for speed-based exploitation.

Recommended articles