How to Scale a Brokerage Infrastructure in Four Practical Phases

Growth stalls when your brokerage infrastructure can't keep up with volume. Latency spikes during volatility, LPs start rejecting flow, and back-office reconciliation goes manual. The cause is almost always an architecture built for a smaller operation that nobody refactored.

Most brokerages try to fix this by upgrading whatever component feels slowest. That rarely works. The bottleneck you notice first is usually a symptom of a deeper scalability constraint, and throwing money at symptoms doesn't solve the underlying problem. Brokerage growth stalls until the root cause gets addressed.

So, how to scale a brokerage infrastructure? This guide breaks the process into four phases: what to measure, what to change, and what the result should look like before you move to the next one.

Key Takeaways

- Scaling starts with measurement: identifying the specific KPIs and bottlenecks that limit throughput before investing in any infrastructure change.

- Execution layer decoupling (separating order routing from the matching engine) is the foundational upgrade that makes every subsequent phase more effective.

- Active-active data center architecture eliminates the failover delays of active-passive setups and adds capacity rather than just redundancy.

- Liquidity expansion and real-time risk management must be implemented together; adding depth without exposure-aware routing creates invisible risk concentration.

- Back-office automation and crypto payment infrastructure are the final phase, extending the throughput gains from Phases 1–3 into settlement, compliance, and treasury operations.

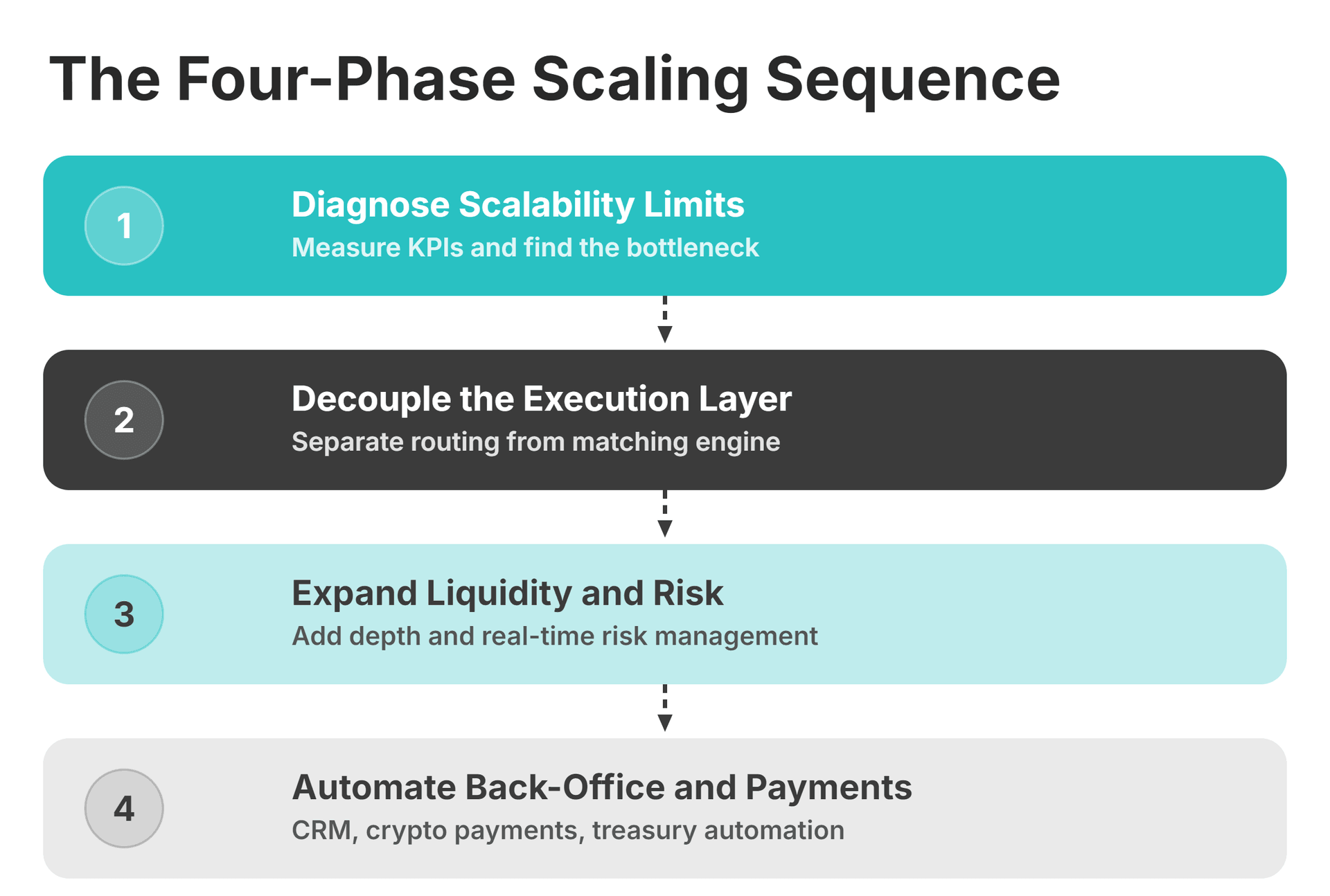

Phase 1: Diagnose Scalability Limits

Upgrading the wrong component wastes capital and delays the fix, so the first step is baselining the system under current conditions to understand your real scalability ceiling. Most brokerages find their actual bottleneck somewhere they didn't expect.

Key KPIs to Monitor

Five metrics tell you where your infrastructure is under pressure:

Order execution latency (P95/P99). Mean latency hides the worst cases. P95 and P99 capture what clients actually see during peak load. Retail execution should stay under 10ms, and institutional or HFT-adjacent flows need sub-1ms. If P99 already sits at 8ms under normal conditions, you have almost no headroom left for volume spikes.

Order rejection rate. LP rejections mean your flow quality no longer matches your routing configuration, or you've outgrown the LP relationships you currently have. Anything above 3–5% needs immediate routing review.

Back-office reconciliation time. If reconciliation takes hours during normal volume, expect days during peak periods. Baseline it now, because you won't get a second chance once volume surges.

Matching engine throughput. Compare your current requests-per-second capacity against peak trading demand. A narrow gap means the matching engine is already your binding constraint.

Settlement cycle time. The US and Canada moved to T+1 settlement in May 2024, and the EU deadline is October 11, 2027. If you built your settlement workflow around T+2, your scaling roadmap needs to account for the shorter cycle now.

Stress-Testing Workloads

KPIs measured under normal load don't show how a brokerage infrastructure behaves under real pressure. Volatility spikes and market open/close windows can push trading volume to 3–5x the intraday average.

Run synthetic workloads at 2x, 5x, and 10x normal throughput. Watch for the first component to break:

- Matching engine saturation

- LP connectivity failures

- Order routing bottlenecks

- Back-office reporting pipeline backlog

Whatever fails first is your actual constraint, and Phase 2 targets it directly.

Record the failure threshold before making any changes. After the upgrade, run the same tests again to confirm the improvement.

Diagnose Before You Scale

B2BROKER's infrastructure audit process identifies your specific throughput constraints before recommending any architecture change.

Phase 2: Decouple and Fortify the Execution Layer

The highest-impact scalability change for most growing brokerages is pulling order routing apart from the matching engine. Once those two components operate independently, every subsequent phase becomes easier to execute.

Abstract Order Routing From Matching

In a tightly coupled architecture, the routing layer and matching engine share state. Because of that, any change to routing logic forces a matching engine restart. Scaling capacity is just as rigid: both components have to grow in lockstep, and a failure in one crashes the other.

Pulling the routing layer into a separate, stateless component solves all of these. You can update routing logic or replace it entirely while the matching engine keeps processing orders. Horizontal scaling works the same way: add capacity to the routing alone. When you onboard a new asset class, the routing configuration plugs into the existing ecosystem without disruption.

Once routing operates independently, you can add intelligence to it. The system starts evaluating available venues in real time and routing algorithms send each order to the venue most likely to deliver the best fill.

B2BROKER built its trading platform around this principle. B2TRADER's matching engine processes 3,000 requests per second with FIX 4.4+ connectivity, and routing abstraction has been part of the architecture from day one.

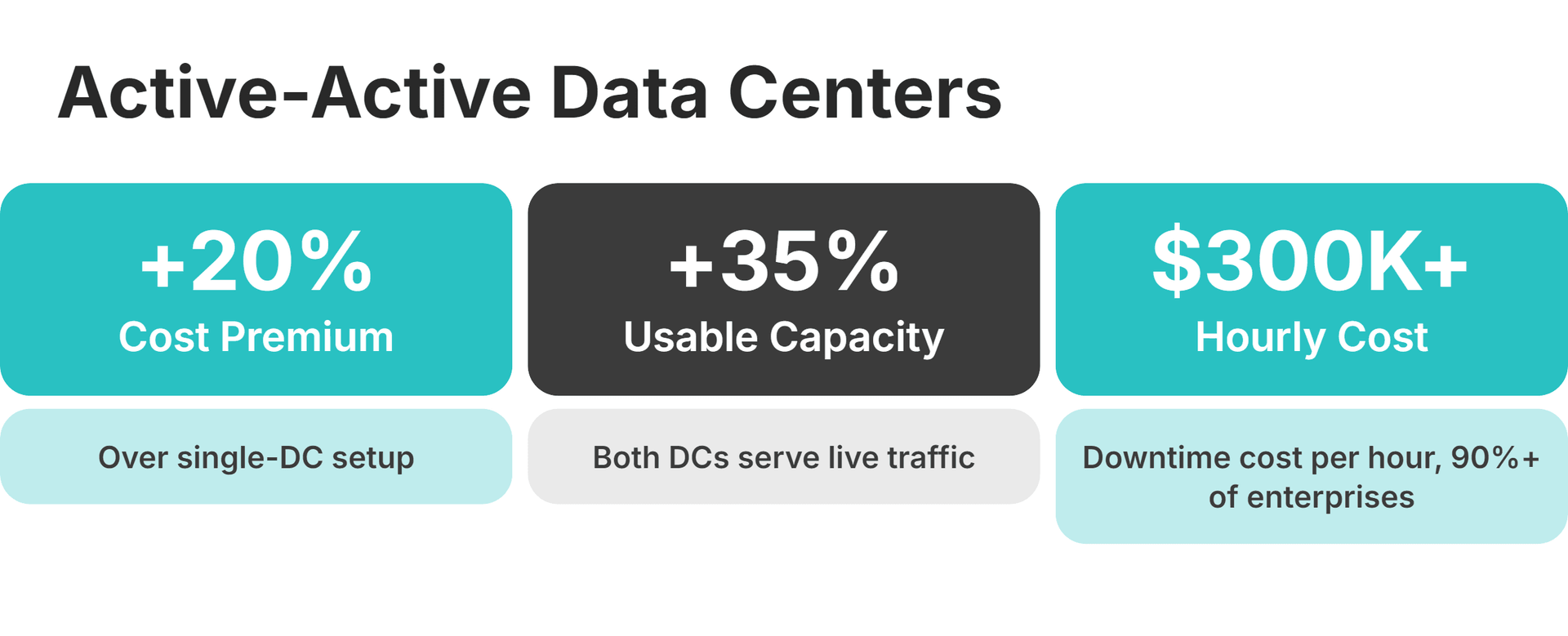

Deploy Active-Active Data Centers

Most brokerages run an active-passive data center architecture by default. One data center handles all live traffic while the second sits idle until failover triggers. When the primary goes down, the switchover takes anywhere from 30 seconds to several minutes, and trading halts completely during that window.

The alternative is running both data centers live at the same time (active-active architecture), with traffic balanced between them. If one data center has an incident, the other absorbs the full load instantly. Capacity decreases, and the platform stays online.

The cost premium runs about 20% above a single-DC setup. In return, you gain a 35% increase in usable capacity because both data centers serve traffic simultaneously. More than 90% of enterprises report hourly downtime costs above $300,000. For any trading system where one outage can exceed that threshold, the additional cost of active-active pays for itself in the first prevented incident.

Phase 3: Expand Liquidity and Real-Time Risk in Tandem

Liquidity expansion and risk management belong in a single phase. Brokerages that add depth before implementing exposure-aware routing create a specific failure mode: more liquidity on paper, but routing logic that still concentrates flow and accumulates invisible risk.

Aggregate Multi-Asset Liquidity Pools

The most direct way to deepen your order books is prime-of-prime aggregation, where multiple Tier 1 provider streams combine into a single feed. For a growing brokerage, the numbers are concrete:

- Spreads tighten by 5–20%

- Fill rates reach 97–99%

- Order rejections drop 30–70% compared to a single-LP setup

Breadth alone doesn't solve the problem, though. Adding more instruments without real depth behind each one leads to execution inconsistency. Thin order books mean large orders move the market against your clients, and that damages trust quickly. The user experience suffers regardless of how polished the front end looks. You need meaningful depth at multiple price levels for every instrument you offer.

Deep liquidity pools are also a prerequisite for the next step. Exposure-aware routing can only function when sufficient depth exists at multiple venues. Take that depth away and the routing logic has nothing to optimize against.

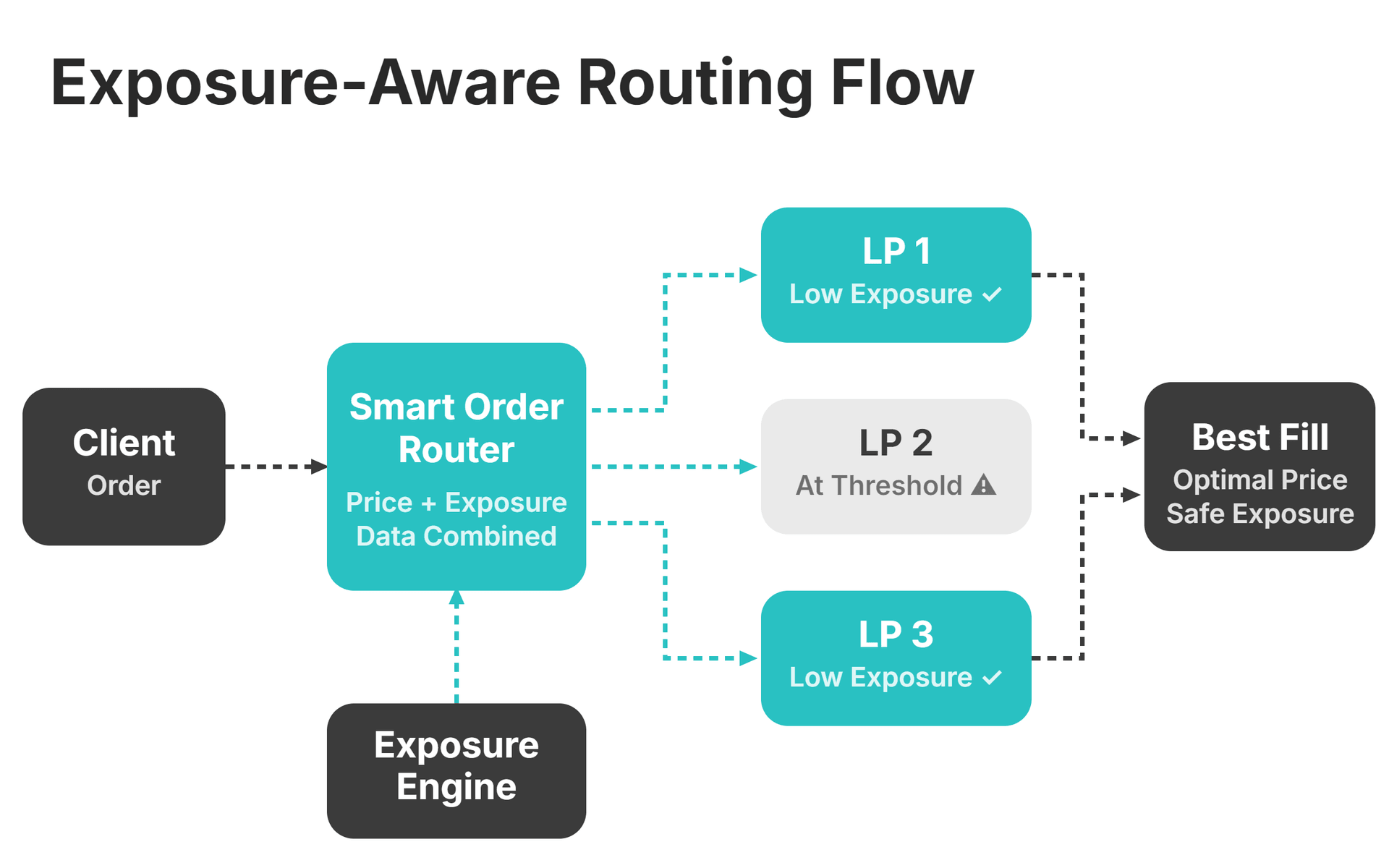

Implement Exposure-Aware Smart Routing

Standard smart order routing picks the venue with the best price, which works until your exposure to a single counterparty starts approaching risk limits. Exposure-aware routing solves that by adding a second input: your current portfolio exposure against each counterparty and LP.

When routing logic can see real-time exposure data, it avoids concentrating flow with counterparties where exposure is already at threshold. Otherwise, a brokerage may technically have liquidity available but cannot safely route to it because doing so would breach risk limits, forcing client order rejections.

Routing logic is only half of the risk picture. The other half is margin monitoring across asset classes. Say a client is long EUR/USD and short BTC at the same time, and those positions partially offset each other. The margin calculation should reflect the net risk of the combined portfolio. If your margin engine runs separately for FX and crypto, it doesn't see that offset. Collateral gets locked in the FX book while the crypto book demands more margin than the client actually needs. Capital efficiency drops and friction on the platform increases.

Add Depth Across Every Asset Class You Offer

Institutional-grade liquidity aggregation across FX, crypto, commodities, and indices through one connection.

Phase 4: Automate Back-Office and Payments

Phases 1–3 address the execution stack. Phase 4 addresses the operational infrastructure underneath it: the CRM, compliance reporting, settlement, and payment workflows that turn matched trades into completed transactions. At scale, manual back-office processes become the binding constraint even when the execution layer is running well. Improving operational efficiency here has a direct impact on profitability.

Consolidate Client Data Into One CRM

Running separate CRM systems per asset class creates a predictable set of problems:

- Client records get duplicated

- KYC status falls out of sync between systems

- Billing can't reconcile when instruments live in separate databases

- Compliance reporting needs manual merging before submission

A unified CRM that brings onboarding, KYC, billing, and reporting under one roof eliminates these problems structurally and helps streamline compliance operations. Every client has one record, regardless of which platform generated the activity. Compliance teams pull reports from the full book in a single query, and billing logic runs once against a complete view of each client's positions.

The back-office upgrade also has a direct impact on regulatory compliance. T+1 settlement requirements demand faster reconciliation workflows than manual processes can support. Automated reconciliation running in real time against a unified data model satisfies T+1 without requiring additional staff.

All-In-One CRM & Back Office for Brokers and Exchanges

Fully Customisable Trader’s Room with Modular Features

Built-In IB Module, KYC, Payment Integrations, and Reporting Tools

Intuitive Interface that Boosts Client Engagement

Introduce Real-Time Treasury and Crypto Payments

Faster reconciliation fixes the data problem, but treasury teams also need real-time visibility into funding. Live dashboards showing positions at every counterparty give risk and finance teams that visibility.

Treasury visibility pairs naturally with crypto settlement, because both address the same bottleneck: moving money faster. The cost advantage is concrete. Settlement fees run approximately 0.5%, compared to 2–3% on traditional payment rails.

For brokerages with clients in multiple jurisdictions, crypto payments also eliminate the cross-border friction that slows traditional wire transfers. Funds move in near real time instead of waiting for banking hours and correspondent bank relationships.

Migration Path to a Modular Usage-Based Stack

The four phases described above assume incremental migration. Most growing brokerages, including smaller ones scaling past initial capacity, can't afford planned downtime to rearchitect the whole stack. You need to upgrade while the system is live.

The guiding principle is straightforward: decouple before you replace. Make each back-end component independently swappable before you actually swap it. That means inserting abstraction layers between tightly coupled components, including API boundaries, event streams, and configuration interfaces. Once those API layers exist, upgrading one service doesn't force changes to every other service around it. Scalability becomes a property of each component individually.

Usage-based infrastructure changes the economics of scaling. Instead of provisioning your matching engine for 10x current load and paying for idle capacity, the system scales horizontally during volume spikes and contracts during quiet periods. This framework turns a fixed-cost infrastructure into a variable one. Capital that would otherwise sit locked in provisioned headroom gets freed up. You can redirect it into deeper liquidity relationships or put it toward licensing and product development, building a more scalable brokerage in the process.

Minimizing Client Downtime

Every migration carries downtime risk. The patterns that reduce it are well-tested.

One proven method is blue-green deployment, where you run old and new infrastructure in parallel and route traffic between them with no gap. If the new component underperforms, you roll back instantly. Feature flags let you shift traffic gradually (5% to the new matching engine, then 25%, then 100%) with monitoring at each threshold before the next step.

The riskiest part of any infrastructure migration is moving the database. Client position data and account state can't have gaps during the switch. Dual-write patterns handle this: you write to both old and new systems simultaneously, so the new system accumulates a full state before you cut over live traffic.

Next Steps to Scale with Confidence

The sequence matters because each phase sets up the next one. You can't expand liquidity until execution routing works properly. You can't automate the back office until you have unified data from the liquidity and risk layer. Start with measurement, move through each phase in order, and the results compound.

The right infrastructure partnership compresses the timeline at every phase. B2BROKER's stack maps directly to the four phases: B2TRADER for matching and execution, institutional liquidity aggregation for FX, crypto, indices, commodities, and metals, B2CORE for unified back-office CRM and compliance, B2COPY for cross-platform copy trading, and B2BINPAY for crypto payment settlement. Every component is purpose-built for brokerages executing this exact migration path.

Map Your Scaling Roadmap to B2BROKER's Infrastructure

From the trading platform to the back office, B2BROKER provides the integrated stack that grows with your brokerage.

Frequently Asked Questions about Scaling a Brokerage Infrastructure

- Does adding more asset classes always improve broker stability, or can it backfire?

It improves stability only if you use a unified infrastructure. Adding asset classes through disconnected systems creates risk blind spots and fragmented liquidity that can actually amplify market volatility.

- What are the biggest risk blind spots brokers face when running separate systems per asset class?

Siloed systems hide total portfolio exposure, allowing correlated drawdowns across different markets to trigger margin calls before your team even notices. They also cause dangerous reconciliation delays and reporting gaps during high-volatility periods.

- How does single-account multi-asset access reduce churn compared to offering separate accounts per asset class?

Forcing traders to open separate accounts for different markets frustrates them and drives them straight to competitors. A unified account keeps all their positions, history, and funding in one place, creating natural friction that prevents them from leaving.

- What are the most common integration mistakes brokers make when expanding to new asset classes?

Brokers often treat expansion as a simple product launch rather than a core infrastructure upgrade, resulting in a patchwork of disconnected systems. They also underestimate the massive back-office burden, as new assets require entirely different KYC, billing, and compliance workflows.

- How do compliance obligations change when a broker adds crypto or commodities to an FX platform?

Each new asset class usually carries entirely distinct licensing and regulatory requirements depending on your operating jurisdiction. For example, crypto often demands separate registrations even if you already hold an active forex license in that same jurisdiction.

Recommended articles