Prime Broker vs. Executing Broker: Which Model Fits Your Firm?

Choosing the wrong broker model is an infrastructure decision that carries capital consequences for years. A firm that signs execution-only relationships when its mandate actually needs consolidated credit across venues ends up carrying bilateral counterparty overhead, and that overhead grows heavier with every venue it adds and every rise in volume.

The model that actually fits comes down to a firm's capital base and technology readiness, plus the regulatory load it can carry. Most firms hit the constraint early, because many banks want to see $50 million or more in monthly volume before they will open a direct tier-1 prime brokerage relationship at all.

This prime broker vs executing broker comparison works as a decision guide rather than a glossary. It weighs prime brokerage against the execution-only and prime of prime alternatives, testing each against those same demands, so a CTO or COO can act on the result directly.

Key Takeaways

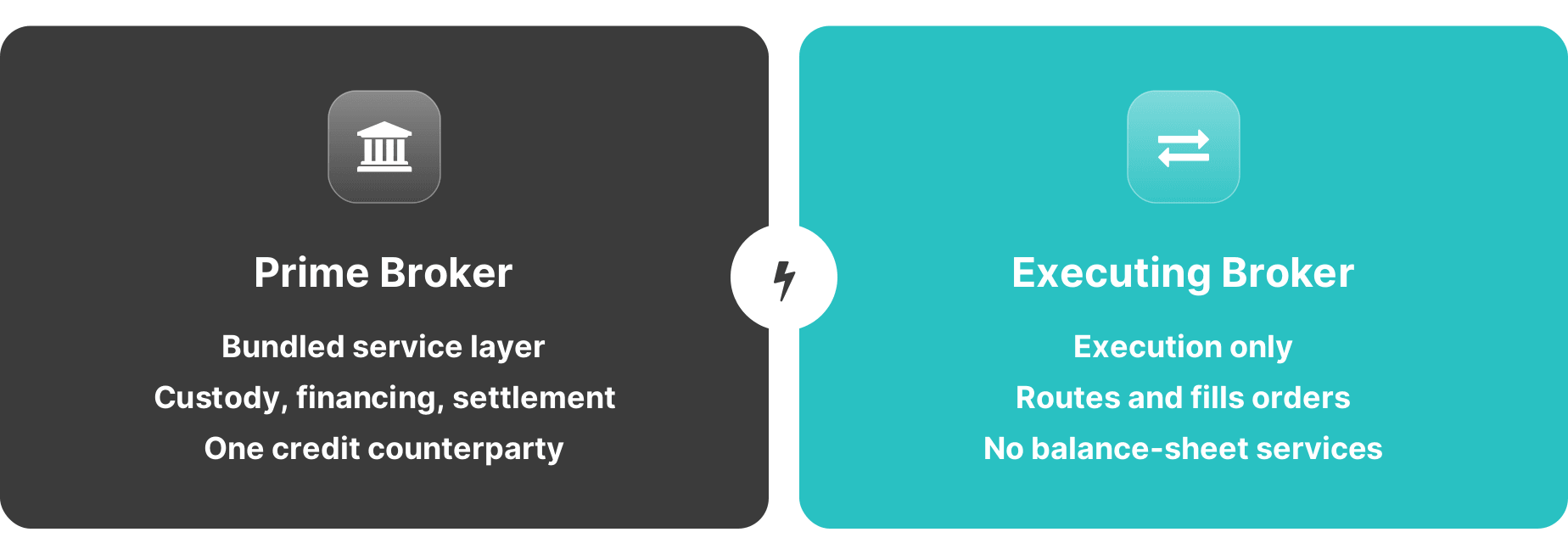

- Prime brokers bundle custody and balance-sheet services under one relationship, while executing brokers concentrate only on order routing and fill quality.

- The model you choose shapes your capital requirements and counterparty exposure, and it dictates the technology stack you have to build or buy.

- Most brokerages cannot meet tier-1 prime brokerage thresholds directly, which makes prime of prime the practical liquidity access point for many firms.

- A mandate that spans several asset classes, from FX to crypto to index products, often needs aggregated liquidity that execution-only relationships cannot support efficiently.

- Regulatory duties diverge sharply between the two models, from reporting and capital-adequacy rules through to counterparty due diligence.

What Is a Prime Broker?

A prime broker provides a bundled institutional service that reaches well beyond executing trades. Under one credit and counterparty relationship, the client gets a full stack of prime brokerage services:

- Custody and securities lending: assets held safe and lent out, the mechanism that also funds client short selling.

- Margin financing: leverage extended against the client's positions.

- Collateral management: pledged assets tracked across venues.

- Consolidated reporting: one netted view of a multi-venue book across global financial markets.

In practice, the prime broker sits between the client and the multiple executing dealers used across venues. When a hedge fund or asset manager trades through a tier-1 prime broker, one of the major investment banks such as Goldman Sachs, JPMorgan Chase, or Morgan Stanley, those trades net and confirm back through that prime broker.

Discover the B2TRADER 2.5 update. Grow your brokerage with Perpetual Futures, advanced CFD capabilities, and an updated data-centric user interface.

16.06.25

Some prime brokers add capital introduction on top, connecting hedge fund clients with the institutional investors that allocate capital. At the clearing and settlement level, each executing dealer that helps execute trades reports its fills to the prime broker, which nets the positions and settles with the client on a net basis.

The client keeps a single margin account and a single settlement counterparty, no matter how many venues handle the actual execution, and reporting arrives in one consolidated stream.

This consolidated structure is why prime brokerage became the standard model for multi-venue institutional mandates. Without it, a firm would negotiate and monitor credit and settlement terms separately with every executing counterparty it uses, and that administrative load climbs with each new dealer it adds.

What Is an Executing Broker?

An executing broker has one precisely defined job in trade execution: it routes and fills orders on behalf of clients. These execution services stop there. Custody and financing sit elsewhere, and so does net settlement, which instead falls to a clearing broker or custodian, or to the client's prime broker if the firm has one.

How a broker routes that flow depends on its model, and the ECN and STP execution models handle it differently. ECN routing sends an order across a network of banks and non-bank market makers that compete on price, sometimes alongside OTC liquidity sources. STP routing passes it straight through to one designated liquidity provider.

That routing choice drives fill quality and rejection rates, and it shapes how spreads behave on FX and CFD instruments once a session turns volatile.

Real-time order flow analysis matters at the institutional level because execution quality shifts from one liquidity provider to the next and moves as the trading day progresses. It changes again with each instrument's volatility.

Execution algorithms slice large trade orders to limit market impact, and a firm that runs execution-only relationships needs analytics that catch any decline in fill quality early, before it turns into a compliance problem or reaches a client.

Prime Broker vs. Executing Broker: Differences for Your Firm

The choice hinges on a single split: a prime broker bundles balance-sheet services under one counterparty, while an executing broker gives you fills and nothing else. The four dimensions below turn that split into criteria you can test your firm against.

Service Scope: Bundled vs. Execution-Only

A prime broker delivers the full-service institutional layer under one relationship, running from custody and financing through consolidated reporting and net settlement, plus additional services such as capital introduction. An executing broker delivers execution and nothing past it.

That concentration cuts the number of vendors a firm has to manage, yet it ties the firm's balance sheet to a single counterparty. If that one provider goes down or changes its credit terms, every bundled function feels the shock at once.

Counterparty Structure and Credit Dependency

In a prime brokerage structure, the prime broker sits in the middle and intermediates credit between the client and every executing dealer. The client then faces one counterparty for margin and settlement, no matter how many venues handle execution.

An execution-only setup pushes that work back onto the firm. Each liquidity provider and executing counterparty becomes a separate negotiated credit relationship the firm has to open and monitor. Run multi-asset flow across ten or more of them, and the credit and collateral tracking alone starts to consume real administrative and risk-management capacity.

Capital Requirements and Balance Sheet Exposure

Direct tier-1 prime brokerage is capital-intensive from the first day. For a forex prime brokerage relationship, many major banks and other financial services firms want to see something like $50 million to $100 million in monthly forex volume before they engage.

On the equities side, the SEC sets a regulatory floor of $500,000 in net equity per prime brokerage account, yet the major banks in practice reserve their balance sheet for far larger hedge funds and pull back from smaller or emerging managers.

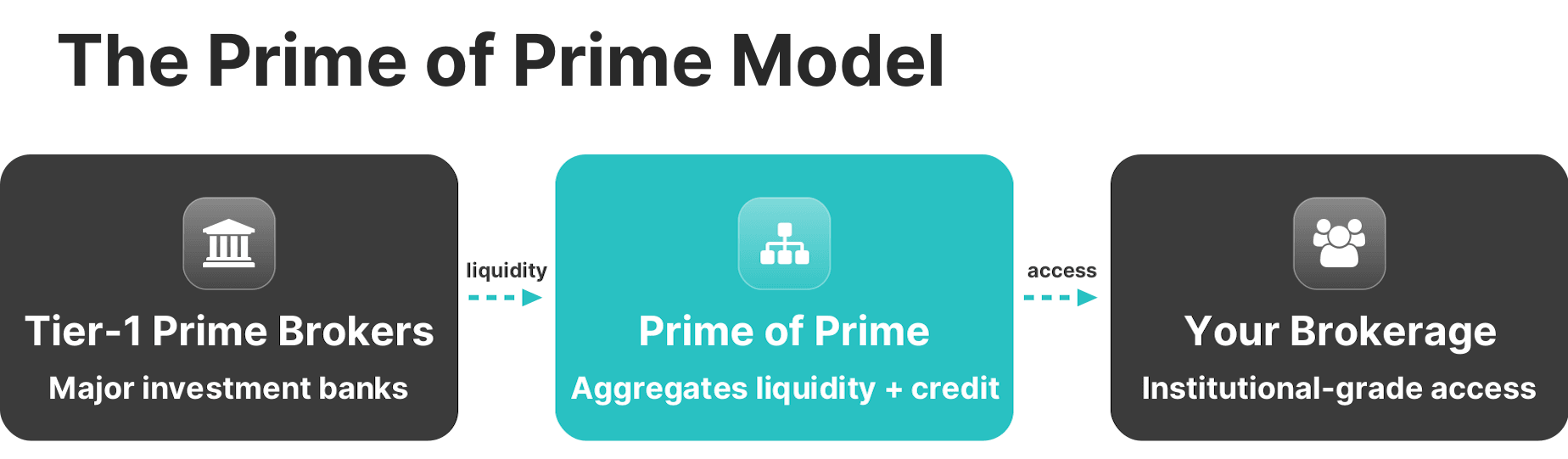

Emerging and mid-size firms rarely clear those bars. That structural barrier is exactly what created demand for the prime of prime model, which opens institutional liquidity access to firms that cannot meet the tier-1 capital and volume requirements on their own.

Target Firm Profile for Each Model

Prime brokerage fits large institutions and institutional investors that run complex, multi-venue mandates and hold the capital base for a direct tier-1 relationship. Think hedge funds and multi-strategy asset managers, plus the major trading operations and trading desks that run their own books across derivatives and cash markets.

Execution brokerage fits firms that source credit and custody on their own and can handle counterparties one at a time. Regional and retail brokers usually sit here, along with single-asset-class operators and the trading platforms that serve individual traders directly.

Find the Liquidity Model That Fits

Our team maps the capital and infrastructure trade-offs to your firm's profile before you commit to a model.

The Prime of Prime Model Explained

Prime of prime (PoP) is an intermediary that keeps a direct relationship with tier-1 prime brokers and passes institutional liquidity access downstream to firms that cannot meet tier-1 thresholds on their own.

It sits between the major bank prime brokers and the end brokerage as a middleman, delivering institutional-grade market access and the core service layer without the capital that a direct relationship demands.

In practice, a PoP provider gives the end-firm four things:

- Multi-asset liquidity aggregated from deep liquidity pools across FX, crypto, indices, commodities, and metals.

- Credit intermediation, so the firm faces one counterparty instead of negotiating bilateral credit with every liquidity provider.

- Consolidated margin netting that works across asset classes.

- Post-trade support that covers reporting and settlement.

This is the practical liquidity model for retail brokerages and regional forex operators, and increasingly for crypto exchanges and fintech platforms moving into multi-asset trading. B2BROKER runs it at institutional scale, with B2CONNECT aggregating multiple LPs and B2TRADER handling matching and execution, plus B2CORE for the back office and CRM.

Infrastructure Requirements by Broker Model

Your broker model decides how much infrastructure you build yourself and how much you source from a vendor, and prime brokerage front-loads the heaviest systems.

Technology Stack for Prime Brokerage Operations

Running prime brokerage operations means standing up several heavy systems, and each one carries its own cost:

- Collateral management that tracks every pledged asset across venues in real time, so the desk always knows what is encumbered.

- Margin financing infrastructure that calculates and processes leverage at the account level.

- Multi-venue connectivity to executing dealers, typically over FIX 4.4/5.0.

- Net settlement infrastructure that reconciles the trade confirmations coming back from many counterparties.

- Real-time risk monitoring that enforces position limits automatically and raises alerts the moment they are breached.

The capital and operational weight of that stack is the reason tier-1 prime brokerage exists as a specialized service, instead of something a broker assembles on its own.

Execution Infrastructure: OMS, EMS, and Matching Engine

Execution infrastructure rests on three components. The Order Management System (OMS) runs the order lifecycle end to end, from creation and modification through to fills and final reconciliation.

The Execution Management System (EMS) handles venue routing in real time, weighing each liquidity provider's price against its available depth and latency to send an order to the best available outcome.

The matching engine is where execution performance is actually decided. B2TRADER's own matching engine, for example, processes 3,000 requests per second on deterministic first-in-first-out queue logic, the kind of throughput and latency profile that institutional execution demands.

When you evaluate an EMS platform, press on three questions:

- What is the documented round-trip latency under peak load?

- What matching logic sits underneath it?

- What reject rate does the LP interface show once conditions turn volatile?

Managing slippage at scale comes down to EMS routing quality and matching-engine latency. Execution infrastructure that cannot hold reject rates low through a volatile session produces slippage that then compounds across every client's flow.

One Engine for Every Market

B2TRADER runs multi-asset flow on a single matching engine, with margin netting and risk controls built in.

Regulatory and Compliance Considerations

In the U.S., an executing broker has to register as a broker-dealer with the SEC and FINRA. That registration brings net capital requirements and customer-protection rules, along with the supervisory duties that come with broker-dealer status.

The SEC's Consolidated Audit Trail (CAT) then requires every order event on NMS securities to be captured and reported, which covers everything from submission and modification to cancellation and fill. At institutional volume, that reporting has to be built into the data infrastructure from the start, because retrofitting it later is slow and expensive.

Prime brokerage sits under a heavier compliance overlay. Capital adequacy falls under SEC Rule 15c3-1, and customer money has to be segregated under Rule 15c3-3. Custody carries its own obligations on top of both. These run as permanent, ongoing costs rather than one-time setup.

The A-Book versus B-Book routing decision feeds directly into this, since how a firm handles its flow determines which capital-adequacy rules apply to the net exposure it keeps.

The two regimes diverge at a glance:

- Executing broker: broker-dealer registration with the SEC and FINRA, net capital rules, and CAT reporting on every order event.

- Prime broker: capital adequacy under Rule 15c3-1, customer-fund segregation under Rule 15c3-3, and custody duties on top.

A firm weighing the prime model should budget for that ongoing compliance load, not only the upfront licensing fee. Execution-only models stay lighter on capital and custody, though they still owe documented best-execution policies and order-level audit trails.

Choosing Your Liquidity Model: Decision Framework

Two questions settle the model for most firms: how many asset classes you cover, and how fast you need to reach the market.

Asset Class Coverage and Venue Requirements

A multi-asset mandate that spans several asset classes, from FX and crypto to CFDs, equity indices, and commodities, needs liquidity aggregated across venues, and those venues differ in how they settle and how their APIs are built.

A single-LP or execution-only arrangement struggles to cover that breadth, because each new venue adds integration work and splinters risk monitoring across disconnected feeds.

PoP aggregation centralizes the LP connections and netting, and it puts risk monitoring back under one roof. A single-asset-class firm with narrow venue needs may do perfectly well on execution-only infrastructure.

Any firm with multi-asset growth plans, though, should settle the liquidity question before the product launches, since fixing it afterward means rebuilding under live traffic.

Deep, Reliable Liquidity Across 10 Major Asset Classes

FX, Crypto, Commodities, Indices & More from One Single Margin Account

Tight Spreads and Ultra-Low Latency Execution

Seamless API Integration with Your Trading Platform

Technology Readiness and Time-to-Market Constraints

Building prime brokerage infrastructure in-house takes at least 12 to 24 months of development. Most brokerages trying to scale in institutional markets simply do not have that runway.

A turnkey ecosystem changes the math and brings time-to-market down from years to weeks. The full checklist for building a forex brokerage lays out everything the ground-up build involves, and shows where an integrated vendor removes the work entirely.

How B2BROKER Resolves the Infrastructure Gap

For a firm that needs institutional-grade liquidity and execution without the capital barrier of a direct tier-1 relationship, B2BROKER's ecosystem closes the compliance and infrastructure gaps the framework above exposes.

B2TRADER's matching engine brings that throughput to your stack, with dynamic leverage and partial liquidation built in and margin netting handled at the account level.

B2CORE runs the back office, from KYC and AML workflows to onboarding automation and the audit trails and document management that compliance teams depend on.

Its API layer connects over FIX 4.4/5.0 as well as REST and WebSocket, linking liquidity providers and EMS to back-office systems in one stack and removing the point-solution vendor sprawl that slows most builds.

Build Your Brokerage on a Solid Foundation

Choosing among the models really comes down to three questions. What service scope does the mandate demand? How much infrastructure can the firm stand up and run? And which regulatory obligations follow from the model?

For most brokerages sitting below the tier-1 capital threshold, prime of prime answers all three at an accessible entry point, giving them consolidated credit and multi-asset liquidity, plus post-trade reporting, without the direct-relationship bar.

An integrated vendor takes most of that build complexity off the table. The pieces that would take years to assemble alone can go live in weeks as one coordinated stack, which is the difference between planning a launch and postponing it.

B2BROKER has operated in this market since 2014, and it now supplies liquidity and technology to more than 1,000 institutional clients worldwide, backed by regulatory licenses across several jurisdictions. That track record is why its infrastructure arrives as a tested stack rather than an unproven build.

Map Your Model to the Stack

Our specialists translate your liquidity model requirements into the infrastructure that can actually support them at scale.

Frequently Asked Questions about Prime Broker vs Executing Broker

- What is the core operational difference between a prime broker and an executing broker?

A prime broker bundles custody and financing together with counterparty intermediation under one relationship, while an executing broker only routes orders and secures fills. That gap sets your capital requirements and the technology stack you have to run.

- When does a brokerage need a prime broker instead of an execution-only relationship?

The need appears once a firm runs multi-venue, multi-asset flow that calls for consolidated credit and net settlement. The usual tipping point is rising volume combined with wider asset coverage and heavier collateral complexity.

- What is prime of prime, and how does it differ from a direct prime brokerage relationship?

An intermediary that holds tier-1 prime broker relationships and passes institutional liquidity and credit downstream to firms that cannot meet tier-1 thresholds directly. It sits between the tier-1 prime broker and the end brokerage, delivering institutional-grade access at a more accessible capital scale.

- How do clearing and settlement responsibilities differ between prime and executing brokers?

In a prime brokerage structure, the prime broker settles with the client on a net basis after the executing dealer fills the trade. An executing broker routes and fills orders, then passes settlement downstream to a clearing broker or custodian.

- What infrastructure does a firm need to support institutional-grade execution and liquidity access?

Execution brokerage needs a high-throughput matching engine and OMS/EMS connectivity, plus real-time risk controls across every asset class it trades. Prime brokerage adds collateral management and margin financing, plus net settlement, on top of that base.